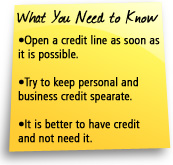

Use an Umbrella in the Sun “A business should try to get a line of credit in place when they don’t really need it, so that it will be there for them when they do,” she says. Weltman says that because a business owner never really knows what the future holds, getting credit early is a must. “As soon as the business is going, you should try for credit. It might be a modest amount at first, but having credit is a way to build up credit, in a sense. Having credit, creating a track record will help the business to qualify for [more] credit.” Don’t Jump in Too Soon “The right time for any business to apply for credit or open a credit account would be … [when] they are able to pay their bills in-full every month and they’re not struggling. Because if they’re struggling already and then they apply for credit they’ll probably be denied credit,” Dunn says. “I think that a lot of [small businesses] try to open credit right away when they first open their business, so they’re not established, they don’t have any credit history and then if [they] go and apply for credit again it will show on [their] credit report that [they] just applied and if it’s not that long—that’s always a negative thing,” Dunn says. “You don’t want to apply over and over for credit.” There are times when a loan may be a better choice for funding purchases, such as equipment or property acquisitions, Weltman says. But when you’re looking for money to help you with working capital, a line of credit would fit the bill. A small business owner may qualify for a line of credit more easily than he or she could for traditional commercial loans, she notes. “I think businesses need credit. That’s really how things work,” she says. “The good thing about a line of credit as opposed to another kind of borrowing is you have that money at your disposal but you’re actually only paying for the amount that you use. If you obtain a $50,000 line of credit, but only use $10,000, you’re only going to be paying interest on the $10,000 and then as you pay it back you have a greater pool to borrow from again. Having a line of credit gives you more control over your money.” Don’t Make It Personal “[Using personal credit] doesn’t help the business build up separate credit and it also may be more costly in terms of interest than what the business rate could be,” Weltman says. “You will want them to be separate, but in the beginning, it won’t be, because you don’t have any other credit,” Dunn says. “Especially if you’re a sole proprietor, when someone checks your business credit, you’re personal credit will come up. “[Small business owners] don’t realize that when you first open a business, your personal credit is your business credit, so if you have bad credit personally, you’ll want to clean that up before you start your business,” she says. Weltman agrees. “The most important thing for a small business owner when it comes to obtaining business credit is to first take care of your personal credit rating and make sure that you clean that up and make sure you have a good personal FICO score,” she says. Small business owners will almost always be required to guarantee the line for their businesses, Weltman says, a fact that many owners are unaware of. Another misconception, she says, is that the owner will not be on the hook for the money. When it comes to small business lines of credit, the owner usually has to guarantee payment. So, many owners are told if they form a corporation or a Limited Liability Company (LLC), they don’t have personal liability, but that doesn’t apply in this situation, she says. In some cases, businesses don’t need credit to sustain operations, but that doesn’t mean that they should disregard the importance of establishing good credit. For these companies, it is still a good idea to create solid credit histories because it gives them additional financial options for the future. “If you have a business for 10 years and you never paid on credit or opened a credit account and then you suddenly need to, that could hurt you,” Dunn says. |

|

|

|||

The first hurdle faced by most small business owners is scraping up enough money to launch and maintain their new ventures. Although some newly established business owners have enough cash on-hand to jumpstart their enterprises and keep them humming along, many rely on credit, whether through the owners’ personal lines or through separate business lines—sometimes both. But how does one decide when it’s the right time to open a line of business credit, and then make the most of a credit line that has been opened?

The first hurdle faced by most small business owners is scraping up enough money to launch and maintain their new ventures. Although some newly established business owners have enough cash on-hand to jumpstart their enterprises and keep them humming along, many rely on credit, whether through the owners’ personal lines or through separate business lines—sometimes both. But how does one decide when it’s the right time to open a line of business credit, and then make the most of a credit line that has been opened?